Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Aug 29, 2025

Week Ahead Economic Preview: Week of 1 September 2025

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

US non-farm payrolls and worldwide PMIs

The coming week builds up to Friday's US non-farm payroll release, set to provide a key signal for Fed policy, but also includes worldwide PMI data from S&P Global as well as the ISM reports and a slew of official data across the world ranging from eurozone inflation to Brazil's GDP.

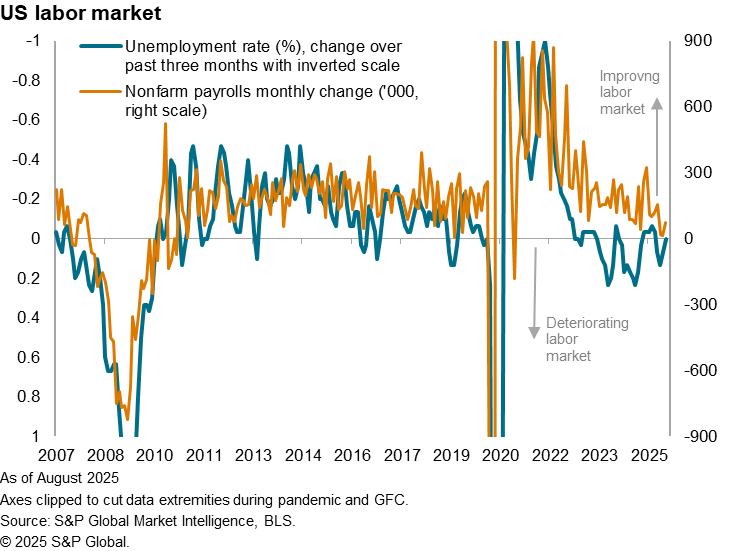

Perhaps the final test for an interest rate cut at the upcoming FOMC meeting in September will be the monthly employment report, and particularly the nonfarm payroll count. The Fed has a dual mandate of promoting maximum employment and ensuring price stability. While it seems to be growing more comfortable with the view that any tariff-related lift in inflation will be modest or temporary, it has grown more concerned about the labour market.

To recap on recent data, the unemployment rate remains low by historical standards, at just 4.2%, but jobs growth has slowed. Just 106k jobs were added in total over the three months to July, making that the worst spell of job creation since 2010 if the pandemic is excluded. Some of this reflects DOGE-related government job losses, but private sector job gains have also been weak, totalling just 155k over the past three months. While this is up from a post-pandemic low of 139k seen in the same period last year, it is low by recent standards: 2023 and 2024 saw 142k jobs added each month on average. Any further disappointment in the August data will fuel rate cut odds after Fed Chair Jerome Powell opened the door to such a move at his Jackson Hole speech.

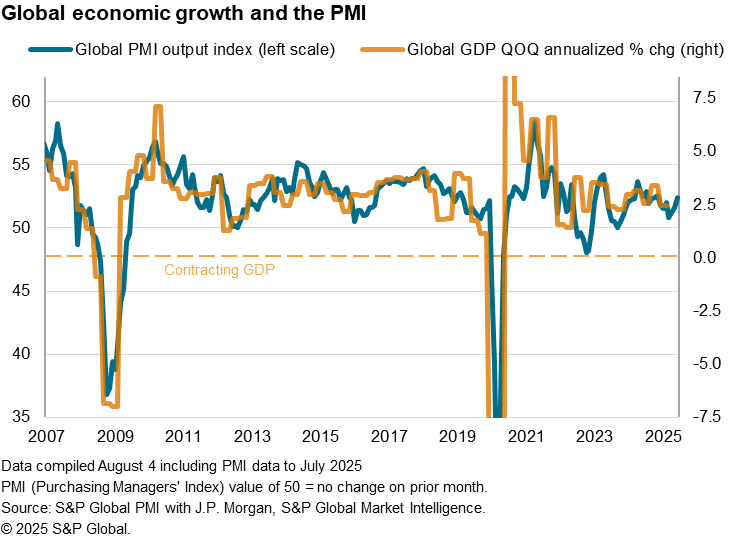

Worldwide PMI data will meanwhile provide an updated view on global economic growth and inflation trends in August. While flash PMI data signalled a broad-based pick up in developed world economic growth in August, some of this looks to have been driven by tariff front running. Emerging market growth had meanwhile weakened slightly in July, as a faster expansion of service sector activity was offset by a renewed, tariff-related, manufacturing downturn.

With August seeing ongoing uncertainties in relation to both sector tariffs and bilateral trade deals with the US, (albeit some concerns around worst case scenarios have eased since April), the performance of manufacturing economies and detailed sector PMI trends will be closely monitored. In addition, broader service sector conditions - which are more closely aligned with financial market conditions in many cases - will provide especially important signals for central bank policy.

The US labour market comes into focus with the monthly employment report.

PMI data will meanwhile provide an update on global economic trends

Key diary events

Monday 1 Sep

US, Canada, Malaysia, Kazakhstan Market Holiday

Worldwide Manufacturing PMIs, incl. global PMI* (released over

September 1-2)

South Korea Trade (Aug)

Australia Building Permits (Jul, prelim)

Indonesia Trade (Jul)

Indonesia Inflation (Aug)

Türkiye GDP (Q2)

United Kingdom Mortgage Lending and Approval (Jul)

Eurozone Unemployment Rate (Jul)

Tuesday 2 Sep

Vietnam Market Holiday

South Korea Inflation (Aug)

Eurozone Inflation (Aug, flash)

Brazil GDP (Q2)

United States ISM Manufacturing PMI (Aug)

Wednesday 3 Sep

Vietnam Market Holiday

Worldwide Services, Composite PMIs, inc. global PMI* (released over

September 3-4)

South Korea GDP (Q2, final)

Australia GDP (Q2)

Türkiye Inflation (Aug)

South Africa GDP (Q2)

United States JOLTs Job Openings (Jul)

United States Factory Orders (Jul)

Thursday 4 Sep

Egypt, Kuwait, Pakistan, UAE Market Holiday

Australia Trade (Jul)

Thailand Inflation (Aug)

Sweden Inflation (Aug, prelim)

Switzerland Inflation (Aug)

Malaysia BNM Interest Rate Decision

Switzerland Unemployment Rate (Aug)

Eurozone Construction PMI* (Aug)

United Kingdom Construction PMI* (Aug)

Eurozone Retail Sales (Jul)

United States ADP Employment Change (Aug)

Canada Trade (Jul)

United States Trade (Jul)

United States ISM Services PMI (Aug)

S&P Global Sector PMI* (Aug)

Friday 5 Sep

Indonesia, Malaysia, Pakistan Market Holiday

Philippines Inflation (Aug)

Germany Factory Orders (Jul)

United Kingdom Retail Sales (Jul)

United Kingdom Halifax House Price Index* (Aug)

France Trade (Jul)

Taiwan Inflation (Aug)

Eurozone GDP (3rd est.)

Canada Unemployment Rate (Aug)

United States Non-Farm Payrolls, Unemployment, Average Hourly

Earnings (Aug)

* Access press releases of indices produced by S&P Global and relevant sponsors here.

What to watch in the coming week

Worldwide PMI data for August

Global manufacturing, services and detailed sector PMI data will be published in the new week for insights into economic conditions after widespread US tariffs kicked into place in August. In particular, any changes to demand, output and price trends will be in focus. This is in addition to scrutinising changes to supply chain conditions. Early flash PMI data indicated that the major developed economies showed resilience in the face of recent geopolitical uncertainty and it will be of interest to study how emerging markets may have performed midway through the third quarter of the year.

Americas: US labour market report, ISM PMI, trade data; Canada trade and employment figures; Brazil GDP

August's labour market report from the US will be the key data highlight in the new week, alongside PMI data from both the Institute for Supply Management (ISM) and S&P Global. August's US Flash PMI data revealed that employment rose for a sixth straight month and at the quickest pace since January, hinting at a positive payroll reading. Broadly, US business activity has also expanded at one of the fastest rates recorded so far this year in August and we await the final data for confirmation of performance.

Separately, Canada also updates employment and trade figures while Brazil publishes second quarter GDP data.

EMEA: Eurozone inflation, retail sales, GDP; UK retail sales, Halifax house prices; Türkiye GDP

Besides the final PMI data, including UK and eurozone construction PMIs, key data in the week for Europe includes official eurozone inflation and retail sales while the UK also publishes retail sales and the Halifax house price index.

The HCOB Eurozone PMI Output Prices Index, which preludes the trend for inflation, has pointed to muted inflation in August and also for the months ahead. Meanwhile, modest services activity growth in August, based on flash PMI data, hints at a slower rise in retail sales. In contrast, a solid expansion in UK services activity points to a potentially stronger year-on-year retail performance amid good weather.

APAC: Australia GDP and trade data; South Korea, Taiwan, Indonesia, Thailand, Philippines, Pakistan inflation; BNM meeting

In addition to PMI data released for the region, key economic releases in APAC include GDP and trade data out of Australia. Additionally, inflation data will be due from various economies while a central bank meeting also takes place in Malaysia, albeit with no change to interest rates expected.

© 2025, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-1-september-2025.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-1-september-2025.html&text=Week+Ahead+Economic+Preview%3a+Week+of+1+September+2025+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-1-september-2025.html","enabled":true},{"name":"email","url":"?subject=Week Ahead Economic Preview: Week of 1 September 2025 | S&P Global &body=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-1-september-2025.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Week+Ahead+Economic+Preview%3a+Week+of+1+September+2025+%7c+S%26P+Global+ http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-1-september-2025.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}