BLOG

May 19, 2021

2020 - Been there, done that! What’s next for the Indian MHCV market in 2021?

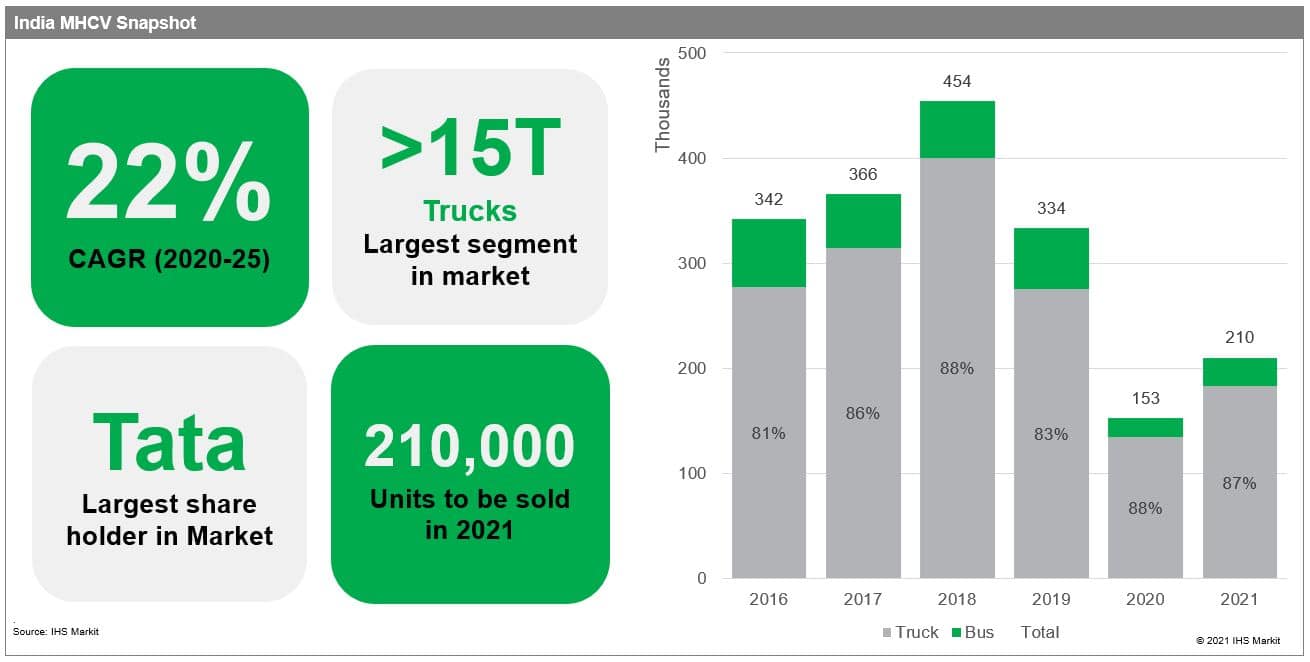

2020 was a year that is forever etched in all our minds. The COVID-19 pandemic forced the Indian government's hand to put the country in a nationwide lockdown for several months spelling doom for the economy's growth. India's GDP contracted 8.2% in 2020 as industries struggled to make ends meet amidst the ever-changing lockdown norms, unavailability of workers, restriction on movement of personnel and material. The Medium and Heavy Commercial Vehicle (MHCV) industry was one of the worst affected industries in the country as April 2020 saw the industry's sales volume at zero for the first time in its reported history. The industry did start recovering in the second half of the year with the third quarter more than quintupling the volume as compared to the second quarter. The fourth quarter yet again doubled the volume from third quarter but even with all these momentous growth figures, the Indian MHCV market ended 2020 at less than half of its 2019 volume, which itself was 26% below the 2018 peak. The Indian MHCV industry sales stood 152,000 units in 2020 as opposed to 333,000 units in 2019.

2020 is now in the past, economic activity has started to pick up pace and so has India's MHCV market. As per the latest Society of Indian Automobile Manufacturers (SIAM) data, the first quarter of 2021 saw 57% higher MHCV sales in India as compared to the previous quarter, but all is not as rosy as it seems. Recently, since mid-April 2021, India has seen a rapid resurgence in COVID-19 cases. The second wave of COVID-19 has already seen daily cases soar to over four times the peak of the first wave but is now starting to show signs of a slowdown as of 11th May 2021. The second wave has forced several state governments to announce lockdown measures for up to 4 weeks and this has also resulted in plant shutdowns at various OEMs. These lockdowns will bog down the economic growth in the immediate future and we estimate the economy to contract this quarter but overall a healthy year-over-year growth of 9.6% will help the economy regain its 2019 size. Industrial activity in the country fell more than 11% in 2020 but is estimated to regain its 2019 levels in 2021. The above-mentioned second wave is sure to delay the recovery of the sector and we estimate some pent-up demand to spill into 2022 as well.

Apart from economic factors, there are several market forces defining the future of India's MHCV market, the most noteworthy of them are as follows:

- India's spending on infrastructure and

construction has been the key driver for growth in the

heavy-duty truck space and it dropped by almost 20% in 2020. Going

forward we estimate India's construction spending to grow 8% in

2021 and another 6% in 2022 as the Government of India has already

announced several large infrastructure projects to the tune of INR

2,00,000 crores (USD 27.4 billion).

- E-commerce Industry is another freight

generating industry and has led the growth of medium-duty truck

segment in India. India's e-commerce industry is expected to be one

of the fastest growing across the globe and the current

government's push on initiatives such as "Digital India", "Make in

India" and others will promote e-commerce activities in India.

Another key development in the process has been the removal of the

limit on FDI in the B2B e-commerce marketplace. We estimate India's

e-Commerce industry to topple its US counterpart and become the

world's second largest by 2034.

- Linked to the above-mentioned factors, India's land

transport demand is estimated to grow more than 50% over

the next 5 years. The government's push to develop better

infrastructure is starting to bear fruit as India's highway network

has grown at a CAGR of 21.4% between 2016 and 2019 and is estimated

to grow at a similar rate until 2025.

- By 2022, the average age of India's MHCV fleet will be

8.2 years and over one 6th of all vehicles plying on Indian roads

will be over 14 years old. An ageing fleet not only is

more polluting but also lacks essential safety features such as ABS

and seat belts. We estimate that several regional directives

banning the use of older highly polluting vehicles will help push

the market for new MHCVs higher and push the replacement

demand.

- Government policies and regulations have been

some of the most prominent factors in defining the Indian MHCV

market's growth in recent years. GST rollout, axle-load norms

revision, BSVI rollout are some of the recent key events in India's

MHCV industry all of which had a huge impact on the market. In the

coming years the government has readied two more such policies to

help the market grow, the scrappage policy and production linked

incentive (PLI) plan.

- The scrappage policy will be rolled out in a phased manner

starting with the first targeting government owned commercial

vehicles (incl. trucks and buses) coming out in April 2022 while

the second phase targeted at privately owned HCVs to start from

April 2023. The government has announced incentives for owners

scrapping their old trucks that include OEM discounts, and taxes

and registration fee waivers. The policy will help create new jobs

and reduce costs for manufacturers by way of recycling metals and

other materials.

- The PLI program is aimed at promoting India as a manufacturing hub for global automotive manufacturers by incentivizing them for increasing production levels. The government has announced a package of over INR570 billion earmarked for the auto industry under the program. The program will help reduce India's import bill as well as increase exports out of the country while creating new jobs as well.

- The scrappage policy will be rolled out in a phased manner

starting with the first targeting government owned commercial

vehicles (incl. trucks and buses) coming out in April 2022 while

the second phase targeted at privately owned HCVs to start from

April 2023. The government has announced incentives for owners

scrapping their old trucks that include OEM discounts, and taxes

and registration fee waivers. The policy will help create new jobs

and reduce costs for manufacturers by way of recycling metals and

other materials.

IHS Markit estimates India's MHCV sales to grow over 35% in 2021 exceeding 210,000 units. Heavy-duty trucks which account for over 55% of the sales in India are estimated to continue their dominance while buses, the worst-affected segment in 2020, are estimated to be the fastest growing due to low base effect. Tata and Ashok Leyland will continue to dominate the market, but Bharat Benz and Eicher are making strong strides and will pose a serious challenge to the stalwarts in the years to come.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmobility%2fen%2fresearch-analysis%2f2020-been-there-done-that-whats-next-for-the-indian-mhcv-mark.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmobility%2fen%2fresearch-analysis%2f2020-been-there-done-that-whats-next-for-the-indian-mhcv-mark.html&text=2020+-+Been+there%2c+done+that!+What%e2%80%99s+next+for+the+Indian+MHCV+market+in+2021%3f+%09+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmobility%2fen%2fresearch-analysis%2f2020-been-there-done-that-whats-next-for-the-indian-mhcv-mark.html","enabled":true},{"name":"email","url":"?subject=2020 - Been there, done that! What’s next for the Indian MHCV market in 2021? | S&P Global &body=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmobility%2fen%2fresearch-analysis%2f2020-been-there-done-that-whats-next-for-the-indian-mhcv-mark.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=2020+-+Been+there%2c+done+that!+What%e2%80%99s+next+for+the+Indian+MHCV+market+in+2021%3f+%09+%7c+S%26P+Global+ http%3a%2f%2fprod.azure.ihsmarkit.com%2fmobility%2fen%2fresearch-analysis%2f2020-been-there-done-that-whats-next-for-the-indian-mhcv-mark.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}