Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Sep 05, 2023

Singapore narrowly averts recession in first half of 2023

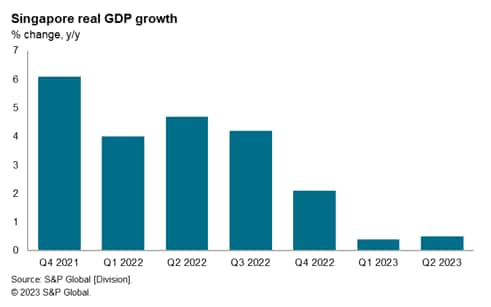

Singapore's second quarter GDP estimate for 2023 was revised down to 0.5% year-on-year (y/y) compared with the advance estimate of 0.7% y/y. Economic growth momentum in 2023 year-to-date has slowed significantly compared with annual GDP growth of 3.6% in 2022. A key factor driving the weakness of economic growth in the first half of 2023 has been weak manufacturing output.

The near-term outlook is expected to remain constrained by weak demand in several important export markets for manufactures, notably the US and European Union (EU), with the pace of recovery in mainland China also weak. The service sector economy is expected to be more resilient, boosted by the continued recovery of international tourism travel in the APAC region.

Singapore economy weakens in first half of 2023

According to the statistics for Q2 2023 GDP released by Singapore's Ministry of Trade and Industry (MTI), Singapore's GDP growth rate was 0.5% y/y, improving on the 0.4% y/y pace in Q1 2023, but much weaker than the 3.6% annual GDP growth rate achieved in 2022.

Measured on a quarter-on-quarter basis (q/q), GDP growth was up 0.1% q/q in the second quarter of 2023, after contracting by 0.4% q/q in the first quarter of 2023. Consequently, Singapore narrowly avoided a technical recession as defined by two successive quarters of contracting quarter-on-quarter GDP.

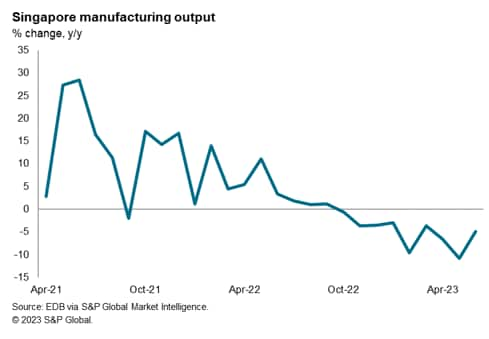

Manufacturing output fell by 7.3% y/y in Q2 2023, following a decline of 5.4% y/y in Q1 2023. Manufacturing output also fell by 1.0% q/q in Q2 2023, after a contraction of 4.6% q/q in Q1 2023.

The construction sector was a bright spot amongst the goods-producing industries, with output up by 6.8% y/y in Q2 2023, after strong growth on 6.9% y/y in Q1 2023 and of 6.7% y/y in calendar 2022.

The service sector also showed positive growth of 2.6% y/y in Q2 2023, with output up 0.8% q/q. The removal of many COVID-19 restrictions since April 2022 and improving tourism flows supported buoyant growth in the accommodation segment, which grew by 13.0% y/y in Q2 2023 after growing by 21.8% y/y in Q1 2023.

International tourism has rebounded, with international visitor arrivals having risen to 1.13 million monthly arrivals in April followed by 1.1 million arrivals in May 2023 and 1.13 million arrivals in June. The tourism rebound has been helped by strong tourism inflows from other APAC nations, notably Indonesia, Malaysia, India and Australia. The number of visitor arrivals is broadly on track to meet the Singapore Tourism Board's target of 12 million tourist visitors in 2023, about double the total tourism arrivals in 2022, which was estimated at 6.3 million.

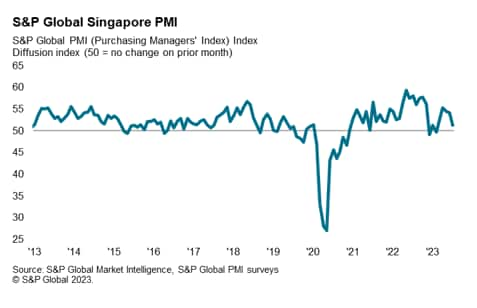

The headline seasonally adjusted S&P Global Singapore Purchasing Manager's Index (PMI) fell sharply in July to 51.3, a steep drop from 54.1 in June. Although the July reading still signalled monthly expansion in private sector activity for the fifth successive month, the pace was the slowest in the current sequence.

Manufacturing sector slowdown continues in early 2023

Latest statistics from Singapore's Economic Development Board showed that manufacturing output continued to weaken in June 2023, declining by 4.9% y/y and by 5.0% month-on-month (m/m). This sharp downturn reflected contraction in output of electronics, chemicals and precision engineering. Electronics output fell by 2.9% y/y while precision engineering output fell by 11.5% y/y. Chemicals output contracted by 8.6% y/y, due to a combination of weak demand and plant maintenance shutdowns.

However, transport engineering showed strong growth of 10.8% y/y, helped by a 6.8% y/y rise in output of the marine and offshore engineering sector, while aerospace engineering was up 16.7% y/y.

Reflecting the weakness of manufacturing sector new orders since mid-2022, Singapore's non-oil domestic exports (NODX) fell by 20.2% y/y in July, following a 15.6% y/y contraction in June, according to latest data released by Enterprise Singapore.

Inflation pressures have eased

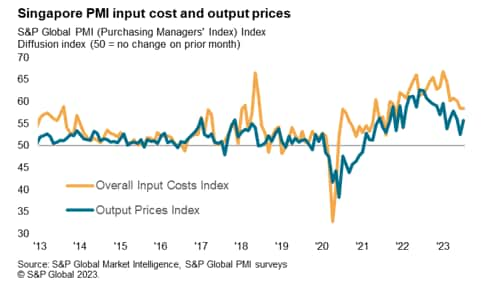

According to the July S&P Global Singapore PMI survey, the rate of input cost inflation was unchanged from June, as higher purchase cost inflation due to rising raw materials, transport and finance fees, offset a slowdown in wage inflation. Firms nevertheless passed on rising costs at a faster rate in July, leading to output price inflation rising further above its series average.

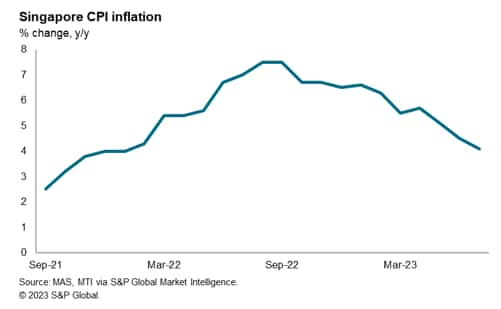

Singapore's headline CPI inflation rate moderated to 4.1% y/y in July compared with 4.5% y/y in June. The Monetary Authority of Singapore (MAS) Core Inflation measure fell to 3.8% y/y in July compared with 4.2% y/y in June.

Headwinds from moderating global electronics demand

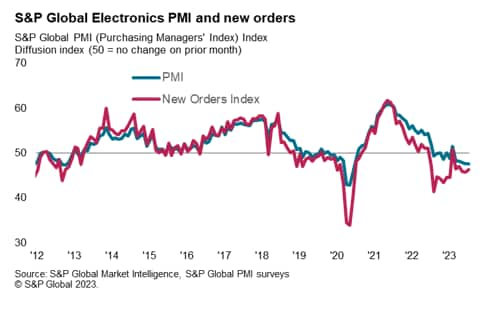

The electronics manufacturing industry is a key segment of Singapore's manufacturing sector, accounting for 40% of the total weight of manufacturing output, dominated by semiconductors-related production. S&P Global survey data since mid-2022 indicates that the global electronics manufacturing industry is continuing to face headwinds from the weak pace of global economic growth.

The headline seasonally adjusted S&P Global Electronics PMI posted 47.6 in July, unchanged on June and continuing to signal moderate contractionary conditions in the global electronics sector.

Weakening global economic growth momentum has impacted on consumer demand for electronics, with soft demand in mainland China also contributing to the downturn in new orders.

Singapore's electronics output fell by 2.9% in June, with electronics output down by 9.8% y/y in the first six months of 2023. Semiconductors output, which accounts for the largest share of total electronics production in Singapore, rose by 3.1% y/y in June, although posting a decline of 9.5% y/y for the first six months of 2023.

Singapore's non-oil domestic exports of electronics continued to show sharp declines in July 2023, falling by 26.1% y/y according to exports data released by Enterprise Singapore. Exports of integrated circuits fell by 35.7% y/y, while exports of PCs fell by 46.1% y/y. Demand for electronics exports has remained weak in key Asian markets, with exports of electronics to mainland China having declined by 26.0% y/y in July, while exports to South Korea fell by 43.8% y/y.

Singapore's economic outlook

After a second year of rapid economic recovery from the pandemic in 2022, economic growth momentum has moderated significantly in the first half of 2023. GDP growth is forecast by S&P Global Market Intelligence to slow to 1.2% in 2023, a significant moderation in growth momentum compared with GDP growth of 3.6% in 2022 and 8.9% y/y in 2021.

Following the release of the revised second quarter GDP statistics, the Ministry of Trade and Industry also lowered its forecast for GDP growth in 2023 from a previous range of 0.5% to 2.5% to a lower range of 0.5% to 1.5%. According to the June 2023 Survey of Professional Forecasters produced by the MAS, the median GDP forecast for 2023 is for growth of 1.4%, significantly lower than the forecast from the March 2023 Survey, which was for GDP growth of 1.9% in 2023.

With continuing headwinds to global growth momentum in 2023 due to very weak growth in the US and EU and sluggish economic recovery in mainland China, the outlook for Singapore's manufacturing sector remains challenging. However, stronger exports of services, notably due to rising international tourist arrivals, will help to mitigate the impact of weaker growth in manufacturing exports.

The increase in Singapore's Goods and Services Tax by 1% from 7% to 8% implemented on 1st January 2023 has also acted as a slight drag on economic growth in 2023, raising fiscal revenue by an estimated 0.7% of GDP per year.

In 2023, taking into account the 1% increase in GST from 1st January 2023, headline and core CPI inflation are projected to average 4.5%-5.5% and 3.5%-4.5% respectively. MAS Core Inflation is projected by the MAS and MTI to moderate in the second half of 2023, as import costs remain low and tightness in the labour market eases. However, the MAS and MTI note upside risks to the inflation outlook from potential shocks to global food commodity prices as well as if persistent tightness in the labour market keeps upward pressures on wage rises.

The medium-term outlook for Singapore's manufacturing sector is supported by a number of positive factors.

Despite near-term headwinds, medium-term prospects for Singapore's electronics industry remains favourable. The outlook for electronics demand is underpinned by major technological developments, including 5G rollout over the next five years, which will drive demand for 5G mobile phones. Demand for industrial electronics is also expected to grow rapidly over the medium term, helped by Industry 4.0, as industrial automation and the Internet of Things boosts rapidly growth in demand for industrial electronics. Singapore also remains an attractive hub for supply chain diversification for some high value-added segments of the electronics industry, as electronics manufacturers continue to diversify their supply chains for production of critical electronics products, notably semiconductors. Reflecting these trends, in 2022, Singapore attracted significant new foreign direct investment inflows into electronics manufacturing.

In the biomedical manufacturing sector, a number of new manufacturing facilities are being built by pharmaceuticals multinationals. This includes a new vaccine manufacturing facility being built by Sanofi Pasteur and a new mRNA vaccine manufacturing plant being built by BioNTech.

The aerospace engineering sector is currently experiencing rapid growth as the reopening of international borders in APAC is boosting commercial air travel across the region. Singapore's role as a leading international aviation hub is likely to continue to strengthen over the medium-term, helped by strong growth in APAC air travel and its role as a key Maintenance, Repair and Overhaul (MRO) hub in APAC.

In the service sector, Singapore is expected to continue to be a leading global international financial centre for investment banking, wealth management and asset management. Singapore will also continue to be a key APAC hub for shipping, aviation and logistics, as well as an important APAC hub for regional headquartering.

However, an important long-term challenge for the Singapore economy will be from ageing demographics. In Budget 2023, the finance minister stated that a key issue for the Singapore economy over the medium to long term will be from demographic ageing, with Singapore having one of the world's fasted ageing populations. The proportion of Singapore's population that is currently aged over 65 years is one-sixth of the population, but this will rise to an estimated one-quarter by 2030. This will result in rising healthcare and social welfare costs and could gradually reduce Singapore's long-term potential GDP growth rate. The role of fiscal policy in addressing demographic ageing will continue to be a key focus for government policy over coming years as the economic impact of demographic ageing intensifies.

Access the Singapore PMI press release here.

Rajiv Biswas, Asia Pacific Chief Economist, S&P Global Market Intelligence

Rajiv.biswas@spglobal.com

© 2023, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fsingapore-narrowly-averts-recession-in-first-half-of-2023-sep23.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fsingapore-narrowly-averts-recession-in-first-half-of-2023-sep23.html&text=Singapore+narrowly+averts+recession+in+first+half+of+2023+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fsingapore-narrowly-averts-recession-in-first-half-of-2023-sep23.html","enabled":true},{"name":"email","url":"?subject=Singapore narrowly averts recession in first half of 2023 | S&P Global &body=http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fsingapore-narrowly-averts-recession-in-first-half-of-2023-sep23.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Singapore+narrowly+averts+recession+in+first+half+of+2023+%7c+S%26P+Global+ http%3a%2f%2fprod.azure.ihsmarkit.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fsingapore-narrowly-averts-recession-in-first-half-of-2023-sep23.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}