Published August 2024

Elemental phosphorus (P4) is the starting material for phosphorus-containing chemicals used in a wide range of industrial markets. The most important chemicals derived directly from P4 are phosphorus trichloride (PCl3), phosphorus pentasulfide, phosphorus pentoxide, and sodium hypophosphite, a relatively small-volume chemical used primarily in electroless nickel plating solutions. Phosphorus trichloride, phosphorus pentasulfide and phosphorus pentoxide are the building blocks for a large number of derivative inorganic and organic chemicals, which in turn are used in a wide variety of high-value specialized applications.

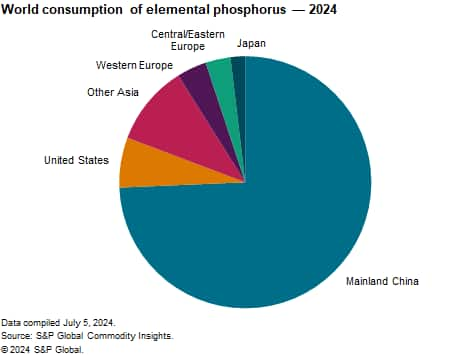

There has been significant rationalization in the phosphorus industry during the past 30 years, largely because of the diminishing use of sodium phosphates in home laundry detergent powders. The phosphorus industry has undergone a dramatic shift away from Western countries to Asian countries during this period, as a result of changes in technology and the increasing cost of electricity. The development of capacity to produce technical-grade phosphoric acid from wet agricultural acid has also resulted in the loss of market share for thermal acid, which is produced from elemental phosphorus. The decline in elemental phosphorus demand resulted in significant capacity decreases in both Europe and North America; Japan ceased yellow phosphorus production entirely in 1987. In contrast, mainland China’s elemental phosphorus capacity has increased rapidly and currently accounts for more than 80% of the global capacity.

The following pie chart shows world consumption of elemental phosphorus:

The production of thermal phosphoric acid remains the largest market for elemental phosphorus. In most regions, industrial phosphates are now made from purified wet phosphoric acid.

After thermal phosphoric acid, phosphorus trichloride is the largest chemical market for elemental phosphorus. Mainland China is again the largest consumer, accounting for more than 70% of the global market. Glyphosate and other pesticide intermediates are by far the largest market for phosphorus trichloride in mainland China; about 80% of the glyphosate produced in mainland China is destined for the export market.

Overall, global consumption of phosphorus chemicals is expected to grow at 2%-3% per year over the forecast period. Thermal phosphoric acid consumption will grow at a slower rate than phosphorus trichloride, where the growth rate is forecast at over 4% per year, driven by vehicle electrification and demand for lithium-ion battery electrification.

For more detailed information, see the table of contents, shown below.

S&P Global Commodity Insights’ Chemical Economics Handbook – Phosphorus and Phosphorus Chemicals is the comprehensive and trusted guide for anyone seeking information on this industry. This latest report details global and regional information, including

Key benefits

S&P Global Commodity Insights’ Chemical Economics Handbook – Phosphorus and Phosphorus Chemicals has been compiled using primary interviews with key suppliers and organizations, and leading representatives from the industry in combination with Commodity Insights’ unparalleled access to upstream and downstream market intelligence and expert insights into industry dynamics, trade and economics.

This report can help you

- Identify trends and driving forces influencing chemical markets

- Forecast and plan for future demand

- Understand the impact of competing materials

- Identify and evaluate potential customers and competitors

- Evaluate producers

- Track changing prices and trade movements

- Analyze the impact of feedstocks, regulations and other factors on chemical profitability